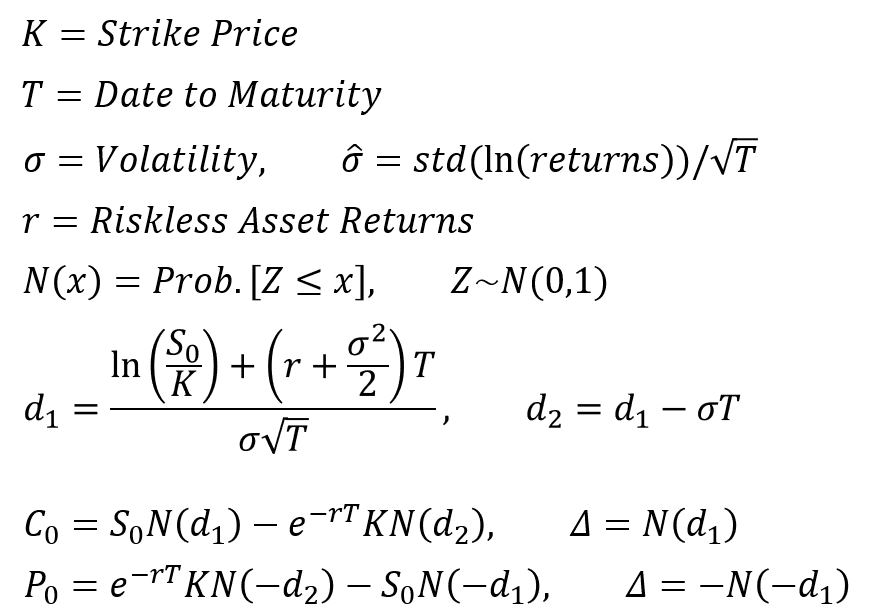

The formula of Black-Scholes is as follow:

I have also written the codes of estimating prices under BS Model:

from scipy import stats

def Black_Scholes(r,sig,S0,K,T,isCall):

# European Option Pricing

d1 = (np.log(S0/K) + (r+sig**2/2)*T)/(sig*np.sqrt(T))

d2 = d1 - sig*np.sqrt(T)

if isCall == True:

C0 = S0*stats.norm.cdf(d1,0,1)-np.exp(-r*T)*K*stats.norm.cdf(d2,0,1)

return C0, stats.norm.cdf(d1,0,1)

else:

P0 = -S0*stats.norm.cdf(-d1,0,1)+np.exp(-r*T)*K*stats.norm.cdf(-d2,0,1)

return P0, -stats.norm.cdf(-d1,0,1)

Keep all the other methods the same with the previous blog, only replace the function to price option under binomial-tree model with the function above, and increase the test period from the range of (2015-07-31, 2015-11-30) to (2015-07-31, 2016-03-22), the results of the prices are stored in this file: binomialResults_Binomial&BS.csv

Visualizing the difference between the two models, and we find that these two models nearly predict the same results:

plt.figure(dpi=200)

plt.title('Binomial Against Black-Scholes Price')

plt.xlabel('Binomial Price')

plt.ylabel('Black-Scholes Price')

plt.xlim(0,0.6); plt.ylim(0,0.6)

plt.plot(df_results.BinomialPrice,df_results.BSPrice,ls=' ',marker='.')

plt.savefig('Binomial Against Black-Scholes Price.png')

diff = df_results.BinomialPrice-df_results.BSPrice

ttest_1sample = stats.ttest_1samp(diff, 0)

Out[1]: Ttest_1sampResult(statistic=2.1480372929383886, pvalue=0.031870221099299899)

Then we may conclude that although slightly different, Binomial-Tree and Black-Scholes Models predict nearly the same prices on 50ETF option from 2015-07-31 to 2016-03-22. Plot Black-Scholes Price against Real Price, and we can find it also significantly underestimates the price of options.

plt.figure(dpi=200)

plt.title('Black-Scholes Price against Real Price')

plt.xlabel('Black-Scholes Price')

plt.ylabel('Real Price')

plt.xlim(0,0.6); plt.ylim(0,0.6)

plt.plot(df_results.BinomialPrice,df_results.Close,ls=' ',marker='.')

plt.savefig('Black-Scholes Price against Real Price.png')

No comments:

Post a Comment